基于趨勢(shì)和季節(jié)性的時(shí)間序列預(yù)測(cè)實(shí)戰(zhàn)

↓推薦關(guān)注↓

本文主要分析時(shí)間序列的趨勢(shì)和季節(jié)性,分解時(shí)間序列,實(shí)現(xiàn)預(yù)測(cè)模型。

時(shí)間序列預(yù)測(cè)是基于時(shí)間數(shù)據(jù)進(jìn)行預(yù)測(cè)的任務(wù)。它包括建立模型來進(jìn)行觀測(cè),并在諸如天氣、工程、經(jīng)濟(jì)、金融或商業(yè)預(yù)測(cè)等應(yīng)用中推動(dòng)未來的決策。

本文主要介紹時(shí)間序列預(yù)測(cè)并描述任何時(shí)間序列的兩種主要模式(趨勢(shì)和季節(jié)性)。并基于這些模式對(duì)時(shí)間序列進(jìn)行分解。最后使用一個(gè)被稱為Holt-Winters季節(jié)方法的預(yù)測(cè)模型,來預(yù)測(cè)有趨勢(shì)和/或季節(jié)成分的時(shí)間序列數(shù)據(jù)。

為了涵蓋所有這些內(nèi)容,我們將使用一個(gè)時(shí)間序列數(shù)據(jù)集,包括1981年至1991年期間墨爾本(澳大利亞)的溫度。這個(gè)數(shù)據(jù)集可以從這個(gè)Kaggle下載,也可以在公眾號(hào):Python學(xué)習(xí)與數(shù)據(jù)挖掘,后臺(tái)回復(fù)【墨爾本】下載,其中包含本文的數(shù)據(jù)和代碼。該數(shù)據(jù)集由澳大利亞政府氣象局托管,并根據(jù)該局的“默認(rèn)使用條款”(Open Access Licence)獲得許可。

導(dǎo)入庫和數(shù)據(jù)

首先,導(dǎo)入運(yùn)行代碼所需的下列庫。除了最典型的庫之外,該代碼還基于statsmomodels庫提供的函數(shù),該庫提供了用于估計(jì)許多不同統(tǒng)計(jì)模型的類和函數(shù),如統(tǒng)計(jì)測(cè)試和預(yù)測(cè)模型。

from datetime import datetime, timedelta

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import statsmodels.api as sm

from statsmodels.tsa.stattools import adfuller, kpss

from statsmodels.tsa.api import ExponentialSmoothing

%matplotlib inline

下面是導(dǎo)入數(shù)據(jù)的代碼。數(shù)據(jù)由兩列組成,一列是日期,另一列是1981年至1991年間墨爾本(澳大利亞)的溫度。

# date

numdays = 365*10 + 2

base = '2010-01-01'

base = datetime.strptime(base, '%Y-%m-%d')

date_list = [base + timedelta(days=x) for x in range(numdays)]

date_list = np.array(date_list)

print(len(date_list), date_list[0], date_list[-1])

# temp

x = np.linspace(-np.pi, np.pi, 365)

temp_year = (np.sin(x) + 1.0) * 15

x = np.linspace(-np.pi, np.pi, 366)

temp_leap_year = (np.sin(x) + 1.0)

temp_s = []

for i in range(2010, 2020):

if i == 2010:

temp_s = temp_year + np.random.rand(365) * 20

elif i in [2012, 2016]:

temp_s = np.concatenate((temp_s, temp_leap_year * 15 + np.random.rand(366) * 20 + i % 2010))

else:

temp_s = np.concatenate((temp_s, temp_year + np.random.rand(365) * 20 + i % 2010))

print(len(temp_s))

# df

data = np.concatenate((date_list.reshape(-1, 1), temp_s.reshape(-1, 1)), axis=1)

df_orig = pd.DataFrame(data, columns=['date', 'temp'])

df_orig['date'] = pd.to_datetime(df_orig['date'], format='%Y-%m-%d')

df = df_orig.set_index('date')

df.sort_index(inplace=True)

df

可視化數(shù)據(jù)集

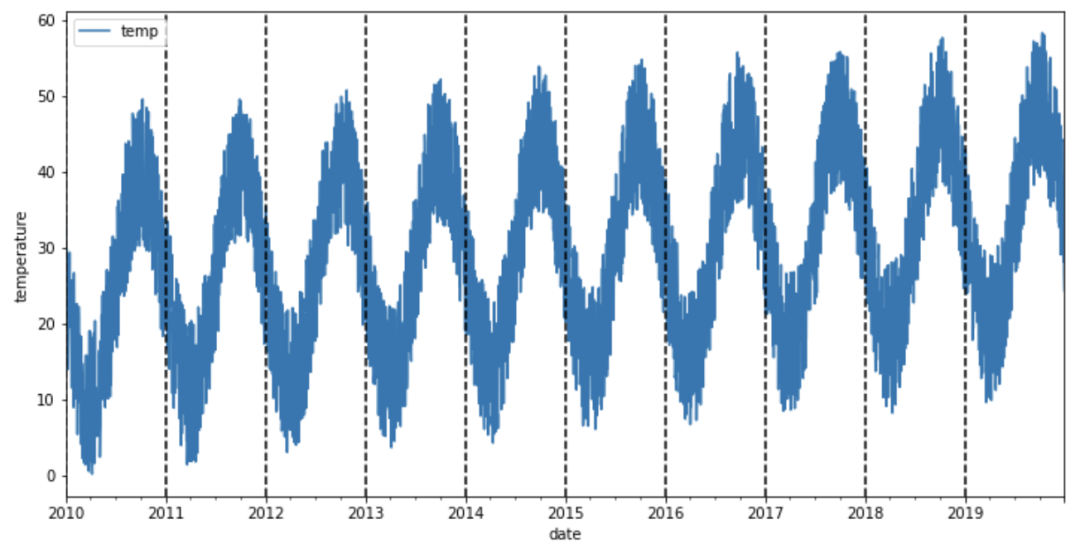

在我們開始分析時(shí)間序列的模式之前,讓我們將每個(gè)垂直虛線對(duì)應(yīng)于一年開始的數(shù)據(jù)可視化。

ax = df_orig.plot(x='date', y='temp', figsize=(12,6))

xcoords = ['2010-01-01', '2011-01-01', '2012-01-01', '2013-01-01', '2014-01-01',

'2015-01-01', '2016-01-01', '2017-01-01', '2018-01-01', '2019-01-01']

for xc in xcoords:

plt.axvline(x=xc, color='black', linestyle='--')

ax.set_ylabel('temperature')

在進(jìn)入下一節(jié)之前,讓我們花點(diǎn)時(shí)間看一下數(shù)據(jù)。這些數(shù)據(jù)似乎有一個(gè)季節(jié)性的變化,冬季溫度上升,夏季溫度下降(南半球)。而且氣溫似乎不會(huì)隨著時(shí)間的推移而增加,因?yàn)闊o論哪一年的平均氣溫都是相同的。

時(shí)間序列模式

時(shí)間序列預(yù)測(cè)模型使用數(shù)學(xué)方程(s)在一系列歷史數(shù)據(jù)中找到模式。然后使用這些方程將數(shù)據(jù)[中的歷史時(shí)間模式投射到未來。

有四種類型的時(shí)間序列模式:

趨勢(shì):數(shù)據(jù)的長期增減。趨勢(shì)可以是任何函數(shù),如線性或指數(shù),并可以隨時(shí)間改變方向。

季節(jié)性:以固定的頻率(一天中的小時(shí)、星期、月、年等)在系列中重復(fù)的周期。季節(jié)模式存在一個(gè)固定的已知周期

周期性:當(dāng)數(shù)據(jù)漲跌時(shí)發(fā)生,但沒有固定的頻率和持續(xù)時(shí)間,例如由經(jīng)濟(jì)狀況引起。

噪音:系列中的隨機(jī)變化。

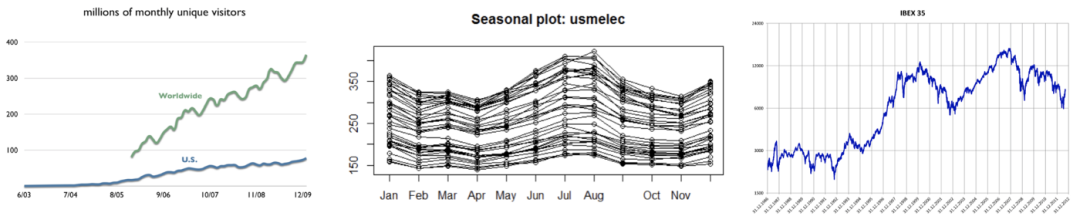

大多數(shù)時(shí)間序列數(shù)據(jù)將包含一個(gè)或多個(gè)模式,但可能不是全部。這里有一些例子,我們可以識(shí)別這些時(shí)間序列模式:

維基百科年度受眾(左圖):在這張圖中,我們可以確定一個(gè)增加的趨勢(shì),受眾每年線性增加。

美國用電量季節(jié)性圖(中圖):每條線對(duì)應(yīng)的是一年,因此我們可以觀察到每年的用電量重復(fù)出現(xiàn)的季節(jié)性。

ibex35的日收盤價(jià)(右圖):這個(gè)時(shí)間序列隨著時(shí)間的推移有一個(gè)增加的趨勢(shì),以及一個(gè)周期性的模式,因?yàn)橛幸恍r(shí)期ibex35由于經(jīng)濟(jì)原因而下降。

如果我們假設(shè)對(duì)這些模式進(jìn)行加法分解,我們可以這樣寫:

Y[t] = t [t] + S[t] + e[t]

其中Y[t]為數(shù)據(jù),t [t]為趨勢(shì)周期分量,S[t]為季節(jié)分量,e[t]為噪聲,t為時(shí)間周期。

另一方面,乘法分解可以寫成:

Y[t] = t [t] *S[t] *e[t]

當(dāng)季節(jié)波動(dòng)不隨時(shí)間序列水平變化時(shí),加法分解是最合適的方法。相反,當(dāng)季節(jié)成分的變化與時(shí)間序列水平成正比時(shí),則采用乘法分解更為合適。

分解數(shù)據(jù)

平穩(wěn)時(shí)間序列被定義為其不依賴于觀察到該序列的時(shí)間。因此具有趨勢(shì)或季節(jié)性的時(shí)間序列不是平穩(wěn)的,而白噪聲序列是平穩(wěn)的。從數(shù)學(xué)意義上講,如果一個(gè)時(shí)間序列的均值和方差不變,且協(xié)方差與時(shí)間無關(guān),那么這個(gè)時(shí)間序列就是平穩(wěn)的。有不同的例子來比較平穩(wěn)和非平穩(wěn)時(shí)間序列。一般來說,平穩(wěn)時(shí)間序列不會(huì)有長期可預(yù)測(cè)的模式。

為什么穩(wěn)定性很重要呢?

平穩(wěn)性已經(jīng)成為時(shí)間序列分析中許多實(shí)踐和工具的常見假設(shè)。其中包括趨勢(shì)估計(jì)、預(yù)測(cè)和因果推斷等。因此,在許多情況下,需要確定數(shù)據(jù)是否是由固定過程生成的,并將其轉(zhuǎn)換為具有該過程生成的樣本的屬性。

如何檢驗(yàn)時(shí)間序列的平穩(wěn)性呢?

我們可以用兩種方法來檢驗(yàn)。一方面,我們可以通過檢查時(shí)間序列的均值和方差來手動(dòng)檢查。另一方面,我們可以使用測(cè)試函數(shù)來評(píng)估平穩(wěn)性。

有些情況可能會(huì)讓人感到困惑。例如一個(gè)沒有趨勢(shì)和季節(jié)性但具有周期行為的時(shí)間序列是平穩(wěn)的,因?yàn)橹芷诘拈L度不是固定的。

查看趨勢(shì)

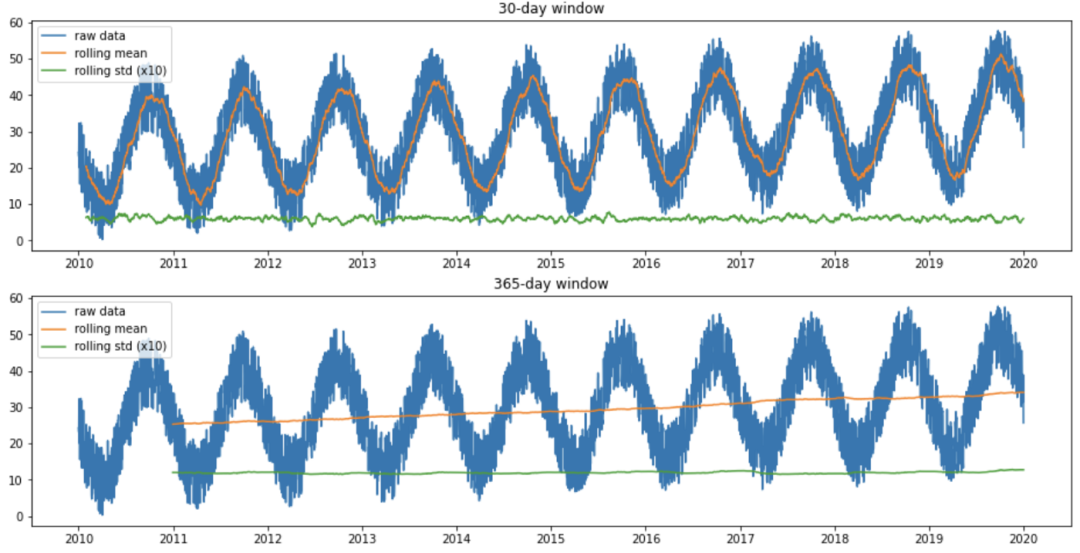

為了分析時(shí)間序列的趨勢(shì),我們首先使用有30天窗口的滾動(dòng)均值方法分析隨時(shí)間推移的平均值。

def analyze_stationarity(timeseries, title):

fig, ax = plt.subplots(2, 1, figsize=(16, 8))

rolmean = pd.Series(timeseries).rolling(window=30).mean()

rolstd = pd.Series(timeseries).rolling(window=30).std()

ax[0].plot(timeseries, label= title)

ax[0].plot(rolmean, label='rolling mean');

ax[0].plot(rolstd, label='rolling std (x10)');

ax[0].set_title('30-day window')

ax[0].legend()

rolmean = pd.Series(timeseries).rolling(window=365).mean()

rolstd = pd.Series(timeseries).rolling(window=365).std()

ax[1].plot(timeseries, label= title)

ax[1].plot(rolmean, label='rolling mean');

ax[1].plot(rolstd, label='rolling std (x10)');

ax[1].set_title('365-day window')

pd.options.display.float_format = '{:.8f}'.format

analyze_stationarity(df['temp'], 'raw data')

ax[1].legend()

在上圖中,我們可以看到使用30天窗口時(shí)滾動(dòng)均值是如何隨時(shí)間波動(dòng)的,這是由數(shù)據(jù)的季節(jié)性模式引起的。此外,當(dāng)使用365天窗口時(shí),滾動(dòng)平均值隨時(shí)間增加,表明隨時(shí)間略有增加的趨勢(shì)。

這也可以通過一些測(cè)試來評(píng)估,如Dickey-Fuller (ADF)和Kwiatkowski, Phillips, Schmidt和Shin (KPSS):

ADF檢驗(yàn)的結(jié)果(p值低于0.05)表明,存在的原假設(shè)可以在95%的置信水平上被拒絕。因此,如果p值低于0.05,則時(shí)間序列是平穩(wěn)的。

def ADF_test(timeseries):

print("Results of Dickey-Fuller Test:")

dftest = adfuller(timeseries, autolag="AIC")

dfoutput = pd.Series(

dftest[0:4],

index=[

"Test Statistic",

"p-value",

"Lags Used",

"Number of Observations Used",

],

)

for key, value in dftest[4].items():

dfoutput["Critical Value (%s)" % key] = value

print(dfoutput)

ADF_test(df)

Results of Dickey-Fuller Test:

Test Statistic -3.69171446

p-value 0.00423122

Lags Used 30.00000000

Number of Observations Used 3621.00000000

Critical Value (1%) -3.43215722

Critical Value (5%) -2.86233853

Critical Value (10%) -2.56719507

dtype: float64KPSS檢驗(yàn)的結(jié)果(p值高于0.05)表明,在95%的置信水平下,不能拒絕的零假設(shè)。因此如果p值低于0.05,則時(shí)間序列不是平穩(wěn)的。

def KPSS_test(timeseries):

print("Results of KPSS Test:")

kpsstest = kpss(timeseries.dropna(), regression="c", nlags="auto")

kpss_output = pd.Series(

kpsstest[0:3], index=["Test Statistic", "p-value", "Lags Used"]

)

for key, value in kpsstest[3].items():

kpss_output["Critical Value (%s)" % key] = value

print(kpss_output)

KPSS_test(df)

Results of KPSS Test:

Test Statistic 1.04843270

p-value 0.01000000

Lags Used 37.00000000

Critical Value (10%) 0.34700000

Critical Value (5%) 0.46300000

Critical Value (2.5%) 0.57400000

Critical Value (1%) 0.73900000

dtype: float64雖然這些檢驗(yàn)似乎是為了檢查數(shù)據(jù)的平穩(wěn)性,但這些檢驗(yàn)對(duì)于分析時(shí)間序列的趨勢(shì)而不是季節(jié)性是有用的。

統(tǒng)計(jì)結(jié)果還顯示了時(shí)間序列的平穩(wěn)性的影響。雖然兩個(gè)檢驗(yàn)的零假設(shè)是相反的。ADF檢驗(yàn)表明時(shí)間序列是平穩(wěn)的(p值> 0.05),而KPSS檢驗(yàn)表明時(shí)間序列不是平穩(wěn)的(p值> 0.05)。但這個(gè)數(shù)據(jù)集創(chuàng)建時(shí)帶有輕微的趨勢(shì),因此結(jié)果表明,KPSS測(cè)試對(duì)于分析這個(gè)數(shù)據(jù)集更準(zhǔn)確。

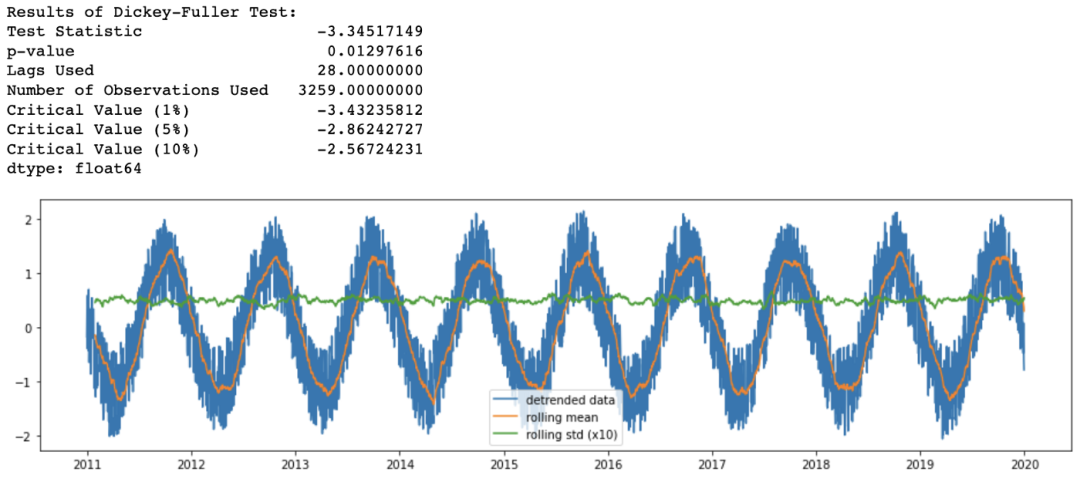

為了減少數(shù)據(jù)集的趨勢(shì),我們可以使用以下方法消除趨勢(shì):

df_detrend = (df - df.rolling(window=365).mean()) / df.rolling(window=365).std()

analyze_stationarity(df_detrend['temp'].dropna(), 'detrended data')

ADF_test(df_detrend.dropna())

檢查季節(jié)性

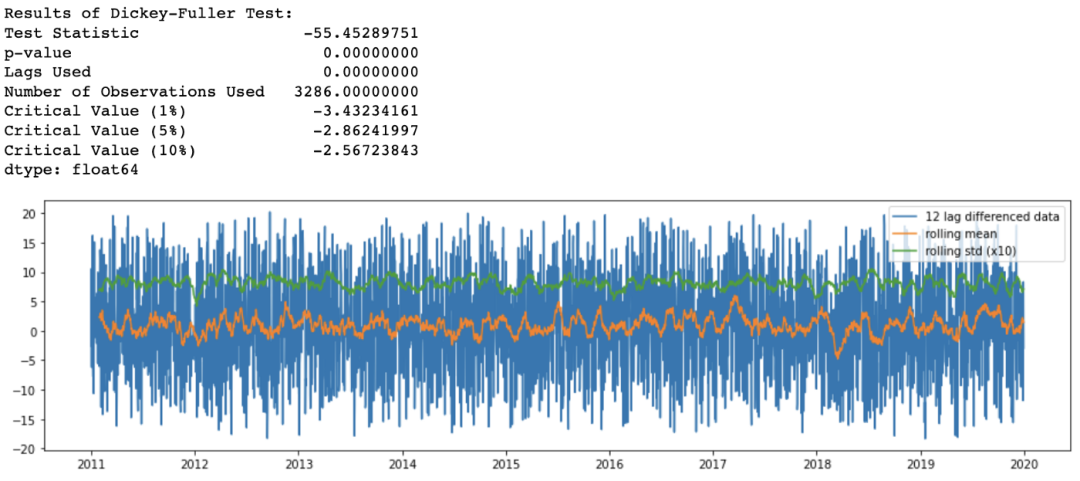

正如在之前從滑動(dòng)窗口中觀察到的,在我們的時(shí)間序列中有一個(gè)季節(jié)模式。因此應(yīng)該采用差分方法來去除時(shí)間序列中潛在的季節(jié)或周期模式。由于樣本數(shù)據(jù)集具有12個(gè)月的季節(jié)性,我使用了365個(gè)滯后差值:

df_365lag = df - df.shift(365)

analyze_stationarity(df_365lag['temp'].dropna(), '12 lag differenced data')

ADF_test(df_365lag.dropna())

現(xiàn)在,滑動(dòng)均值和標(biāo)準(zhǔn)差隨著時(shí)間的推移或多或少保持不變,所以我們有一個(gè)平穩(wěn)的時(shí)間序列。

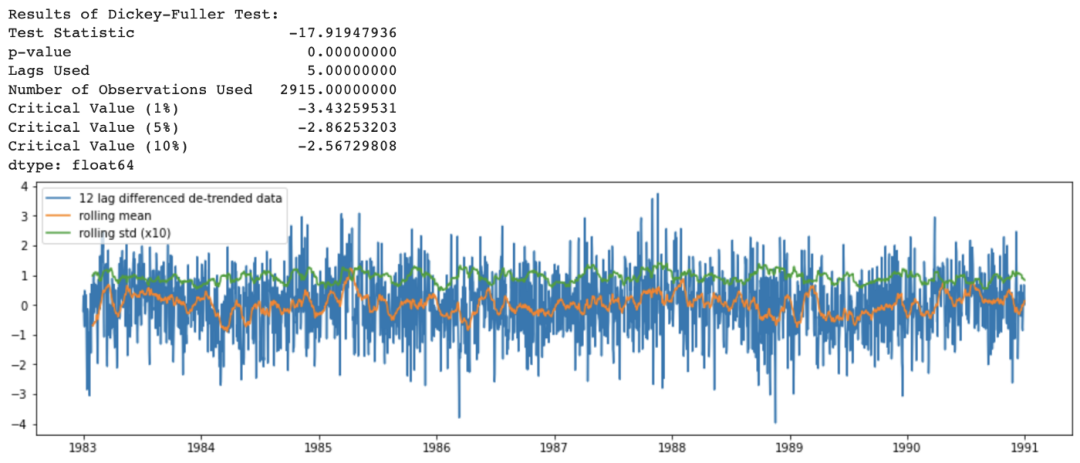

上面方法合在一起的代碼如下:

df_365lag_detrend = df_detrend - df_detrend.shift(365)

analyze_stationarity(df_365lag_detrend['temp'].dropna(), '12 lag differenced de-trended data')

ADF_test(df_365lag_detrend.dropna())

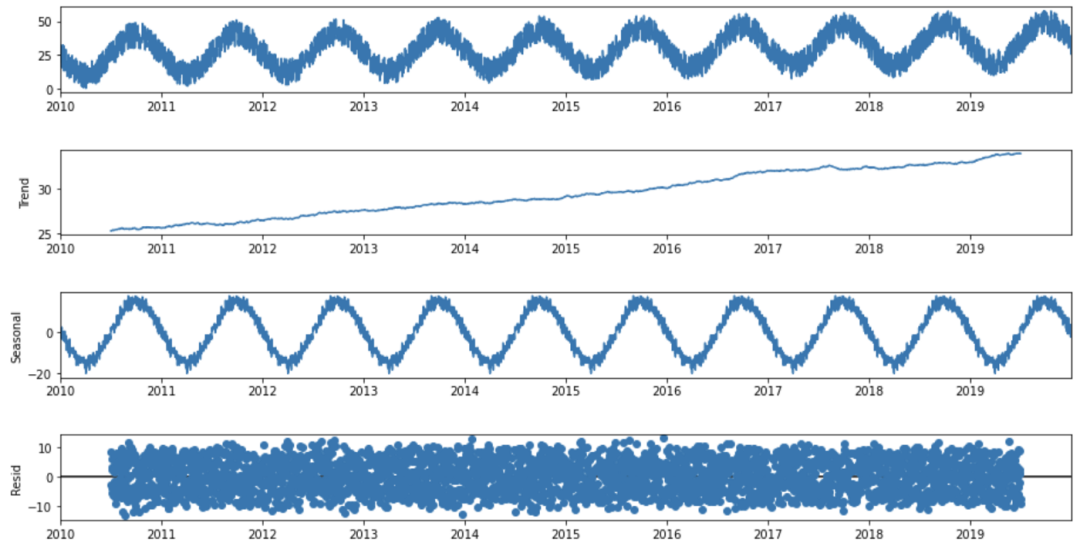

分解模式

基于上述模式的分解可以通過' statmodels '包中的一個(gè)有用的Python函數(shù)seasonal_decomposition來實(shí)現(xiàn):

def seasonal_decompose (df):

decomposition = sm.tsa.seasonal_decompose(df, model='additive', freq=365)

trend = decomposition.trend

seasonal = decomposition.seasonal

residual = decomposition.resid

fig = decomposition.plot()

fig.set_size_inches(14, 7)

plt.show()

return trend, seasonal, residual

seasonal_decompose(df)

在看了分解圖的四個(gè)部分后,可以說,在我們的時(shí)間序列中有很強(qiáng)的年度季節(jié)性成分,以及隨時(shí)間推移的增加趨勢(shì)模式。

時(shí)序建模

時(shí)間序列數(shù)據(jù)的適當(dāng)模型將取決于數(shù)據(jù)的特定特征,例如,數(shù)據(jù)集是否具有總體趨勢(shì)或季節(jié)性。請(qǐng)務(wù)必選擇最適數(shù)據(jù)的模型。

我們可以使用下面這些模型:

Autoregression (AR) Moving Average (MA) Autoregressive Moving Average (ARMA) Autoregressive Integrated Moving Average (ARIMA) Seasonal Autoregressive Integrated Moving-Average (SARIMA) Seasonal Autoregressive Integrated Moving-Average with Exogenous Regressors (SARIMAX) Vector Autoregression (VAR) Vector Autoregression Moving-Average (VARMA) Vector Autoregression Moving-Average with Exogenous Regressors (VARMAX) Simple Exponential Smoothing (SES) Holt Winter’s Exponential Smoothing (HWES)

由于我們的數(shù)據(jù)中存在季節(jié)性,因此選擇HWES,因?yàn)樗m用于具有趨勢(shì)和/或季節(jié)成分的時(shí)間序列數(shù)據(jù)。

這種方法使用指數(shù)平滑來編碼大量的過去的值,并使用它們來預(yù)測(cè)現(xiàn)在和未來的“典型”值。指數(shù)平滑指的是使用指數(shù)加權(quán)移動(dòng)平均(EWMA)“平滑”一個(gè)時(shí)間序列。

在實(shí)現(xiàn)它之前,讓我們創(chuàng)建訓(xùn)練和測(cè)試數(shù)據(jù)集:

y = df['temp'].astype(float)

y_to_train = y[:'2017-12-31']

y_to_val = y['2018-01-01':]

predict_date = len(y) - len(y[:'2017-12-31'])

下面是使用均方根誤差(RMSE)作為評(píng)估模型誤差的度量的實(shí)現(xiàn)。

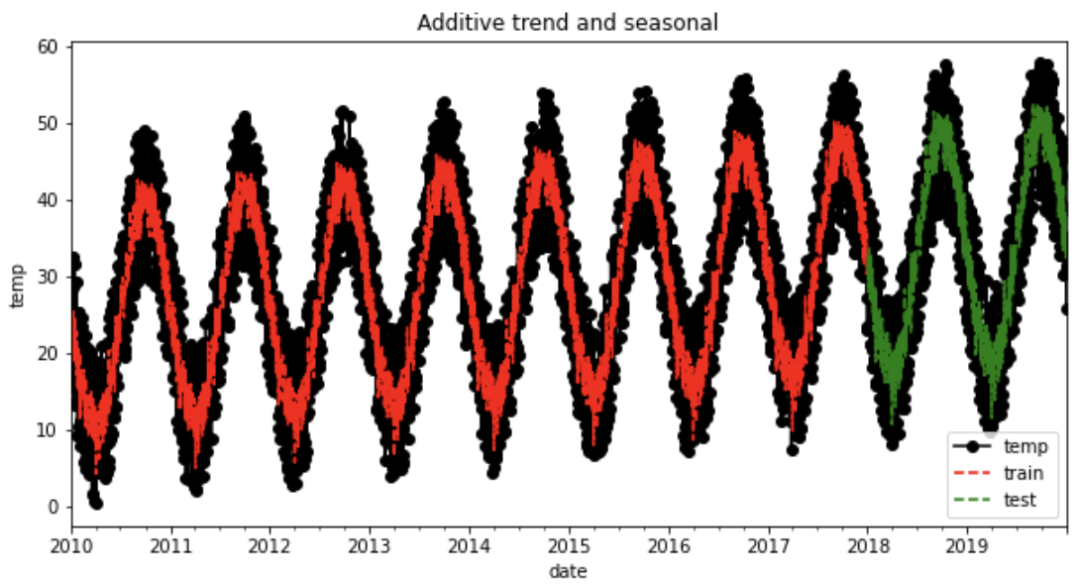

def holt_win_sea(y, y_to_train, y_to_test, seasonal_period, predict_date):

# 完整數(shù)據(jù)和代碼,在公眾號(hào)「機(jī)器學(xué)習(xí)研習(xí)院」后臺(tái)回復(fù)【墨爾本】獲取

fit1 = ExponentialSmoothing(y_to_train, seasonal_periods=seasonal_period, trend='add', seasonal='add').fit(use_boxcox=True)

fcast1 = fit1.forecast(predict_date).rename('Additive')

mse1 = ((fcast1 - y_to_test.values) ** 2).mean()

print('The Root Mean Squared Error of additive trend, additive seasonal of '+

'period season_length={} and a Box-Cox transformation {}'.format(seasonal_period,round(np.sqrt(mse1), 2)))

y.plot(marker='o', color='black', legend=True, figsize=(10, 5))

fit1.fittedvalues.plot(style='--', color='red', label='train')

fcast1.plot(style='--', color='green', label='test')

plt.ylabel('temp')

plt.title('Additive trend and seasonal')

plt.legend()

plt.show()

holt_win_sea(y, y_to_train, y_to_val, 365, predict_date)

The Root Mean Squared Error of additive trend, additive seasonal of period season_length=365 and a Box-Cox transformation 6.27

從圖中我們可以觀察到模型是如何捕捉時(shí)間序列的季節(jié)性和趨勢(shì)的,在異常值的預(yù)測(cè)上則存在一些誤差。

總結(jié)

在本文中,我們通過一個(gè)基于溫度數(shù)據(jù)集的實(shí)際示例來介紹趨勢(shì)和季節(jié)性。除了檢查趨勢(shì)和季節(jié)性之外,我們還看到了如何降低它,以及如何創(chuàng)建一個(gè)基本模型,利用這些模式來推斷未來幾天的溫度。

了解主要的時(shí)間序列模式和學(xué)習(xí)如何實(shí)現(xiàn)時(shí)間序列預(yù)測(cè)模型是至關(guān)重要的,因?yàn)樗鼈冇性S多應(yīng)用。

長按或掃描下方二維碼,后臺(tái)回復(fù):加群,即可申請(qǐng)入群。一定要備注:來源+研究方向+學(xué)校/公司,否則不拉入群中,見諒!

(長按三秒,進(jìn)入后臺(tái))

推薦閱讀